Excellent credit can make it easier for you to qualify for the finest credit cards, mortgages, and competitive loan rates, which can ultimately save you money. The best credit ratings are those that are “Excellent.”

A strong credit rating can help you avoid paying a ton of money in interest throughout your life. You might be able to avoid certain expenses as a result.

For instance, if you took out a personal loan, having a good credit score may enable you to avoid paying personal loan origination fees, which are costs incurred during the loan application process.

Why It Matters to Have a Good Credit Score

Lenders base their decision on how hazardous a borrower you could be on your credit score, which is a three-digit figure.

You have a better chance of getting approved for a loan and getting the best interest rate if your credit score is higher. In general, those with strong credit are given the best interest rates and loan conditions (670 or higher).

Unfortunately, many banks have restrictions on issuing loans for people who are unemployed, people which is a rather negative factor in society.

If your credit score is low (below 580) or your credit history is short, you might not be able to fulfill a lender’s minimum credit scoring standards. You may be unable to obtain the money you require as a result.

You might be able to get approved for a loan if you apply with a co-signer or co-borrower, or you might look into personal loans for those with terrible credit.

Is It Feasible to Have the Highest Credit Score?

Experian believes that just 1.2% of people have a credit score of 850, which is excellent. A perfect score is challenging to get and even more challenging to retain, yet being feasible.

There Are no Negative

Your credit record must be flawless, just as the word “perfect” suggests. Including missing or late payments. There can never be a late payment on any of your twelve accounts, which include loans and credit cards.

With a weight of 35%, payment history is the most crucial component for determining a FICO credit score, although it has less of an impact on a VantageScore.

Maintain a Modest Credit Use Rate

Both scoring models strongly consider this element. Start by totaling up the credit limits on all of your credit cards to get an idea of your current utilization rate.

Consider that you have two credit cards, one with a $2,000 limit and the other with a $3,000 maximum. You now have access to a total of $5,000 in credit.

The percentage is then calculated by multiplying the current total balances (what you owe) by the available credit and dividing the result by 100.

If you have $1,000 in unpaid bills, your usage rate would be 20% since $1,000 divided by $5,000 is 0.20.

Receive the Mortgage Rate With the Lowest APR

Your mortgage is the loan on which you should focus on obtaining the lowest interest rate feasible given the amount of money involved.

Even a modest percentage increase over the life of your loan may cost you tens of thousands of dollars, so it’s worth the extra effort to shop around and bargain.

A critical phase of the home-buying process is preparing your credit for a mortgage.

Try to Have Your Credit Card Interest Rates Reduced

Your credit card APR is meaningless if you make full monthly payments on your credit card debt.

However, if you have a balance, having a high credit score may aid you in your discussions with the lender to reduce the interest rate. You may spend a lot less money if you can get a lower interest rate.

What Is the Best Credit Rating?

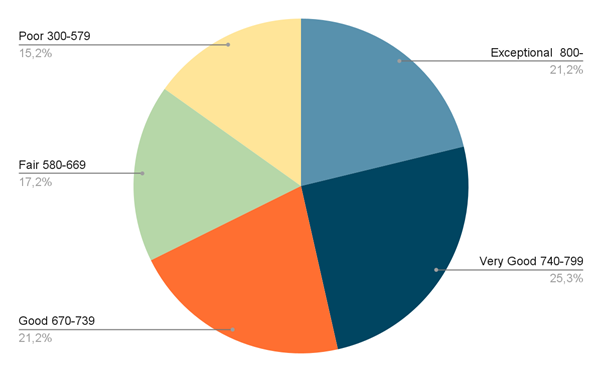

Although there are several kinds of credit scores, the two most prominent ones, FICO and VantageScore, share the same range, from 300 to 850.

A FICO score of 800 is deemed exceptional, while “very good” FICO scores fall between 740 and 799, “good” FICO scores fall between 670 and 739, and “fair” FICO scores fall between 580 and 669.

Poor is defined as a score of less than 580. While a sizable 21% of customers have a credit score of 800 or above and are considered to be “good,”.

The “good” range, according to FICO, is between 670 and 739 on a scale of 300 to 850 for the base FICO Scores. The range of the sector-specific FICO credit ratings is variable, going from 250 to 900.

The intermediate categories, however, are divided into the same groups, and a “good” FICO Score for that industry is still between 670 and 739.

A flawless score won’t always result in lower interest rates than a “very excellent” one, even though it might affect how your fiancé feels about you.

How to Maintain a High Credit Score

The fact that many of the same tactics used to raise your credit score are also employed to keep it high may not come as a surprise to you.

Naturally, these tactics have a direct connection to the elements that go into your final score. For instance, about 35% of your credit score is determined by how promptly you pay your payments.

Maintaining a high credit score may be possible by enrolling in automated payments to prevent lost or late payments.

A similar factor that contributes 30% to your credit score is your credit usage, which is the ratio of your entire accessible credit to your total debt.

You may maintain a good credit score by maintaining minimal balances because doing so increases your credit usage.

Conclusion

A perfect or almost perfect score is lovely, but it means virtually nothing save being a badge of pride that only around 1% of people can obtain.

Lenders consider you to be a low credit risk once your score reaches and stays at 780 or above.

In addition to receiving the greatest interest rates and product offerings, you can pretty much count on getting approved for whatever loan you request as long as it is in line with your income level.